Do you have the final say whether or not your insurance company can decide to settle a claim? This provision, otherwise known as consent to settle is found in your medical malpractice insurance policy that requires an insurer to seek an insured’s approval prior to settling a claim for a specific amount.

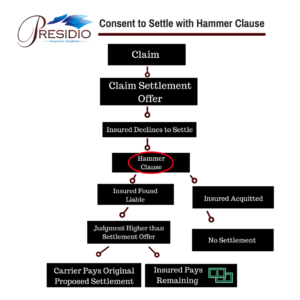

What happens when you have a Consent to Settle with Hammer Clause? Well, after you decline the initial proposed settlement offer the Hammer Clause goes into effect.

Here’s where a Hammer Clause comes into play: It states if a doctor decides to go to court and is found liable then the doctor can be on the hook for the remainder beyond the Hammer Clause amount.

Check out the graphic below for a visual of the Hammer Clause chain of events:

Hammer Clause forces you to comply with your insurance company’s decision to settle the claim, regardless of its merit. Declining to settle, holds you responsible for any costs incurred above the initial settlement amount. For instance, if the plaintiff in a case wants $200,000 to settle a claim and you don’t accept the offer, despite the insurance company’s request in doing so, you’re will be held personally liable for any judgment awarded in excess of the $200,000 when this case goes to trial.

Consequences:

Ignoring a hammer clause opens you up to a serious financial risk. Although every policy doesn’t have a Hammer Clause it is important to note whether or not you are subject to one.