Claims-Made

Claims-made coverage responds to claims based on when the claim is made against an insured. For example, if a claim is made in 2012, based on treatment rendered in 2010, the 2012 claims-made policy responds, as long as the incident occurred after the policy’s retroactive date. The policy’s retroactive date is the date after which treatment must occur to trigger coverage.

Though the above distinction might seem like an insurance technicality, the reality is that selecting your policy type is one of the most significant decisions you’ll make when buying professional liability coverage.

“Tail” Coverage: Because claims-made policies do not cover claims made after the termination of the policy, you must secure “tail” coverage (an extended reporting endorsement) at the termination of the policy. This can happen in many situations such as leaving practice, taking a significant amount of time off, entering a practice that requires you to join a group policy, or moving to a state that will not cover your practice from the prior state. Tail coverage is generally expensive, and some companies will provide free tail coverage in the event of death, disability, or retirement.

What is Occurrence coverage?

An Occurrence policy protects you from any covered incident that “occurs” during the policy period, regardless of when a claim is filed.

An Occurrence policy will respond to claims that are made – even after the policy has been canceled – as long as the incident occurred during the period in which coverage was in force.

In effect, an Occurrence policy offers coverage after the policy ends for incidents that occur during the policy period.

Timing and Limits

Coverage is triggered the moment treatment occurs, regardless of when an eventual claim is made. For example, if a claim is made today based on treatment rendered in 2016, the 2016 Occurrence policy responds.

The Occurrence form provides coverage when the policy is in force and after the cancellation of the policy as long as the claim(s) reported were for incidents that occurred within the coverage dates.

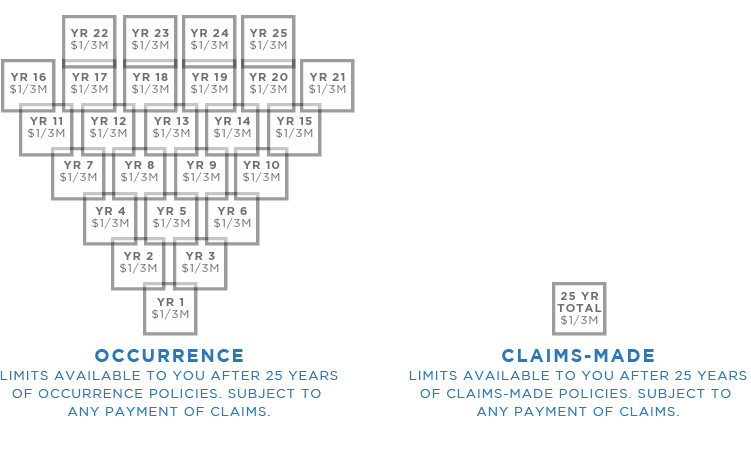

Occurrence coverage remains available for incidents and/or claims which happened while the policy was in force. The limits never expire, subject to the payment of any claims.

Tail

You don’t need to buy tail coverage with an Occurrence policy.

The limits from your previous policy years remain in place to pay any future claims after the end of the policy (subject to the payment of any claims).

MedPro offers doctors the chance to convert their claims-made policies to occurrence. For more information click here.

To get an occurrence quote call Presidio at 805-499-7300 or visit us here.